How Data is the Spinal Cord of the Insurance Lifecycle

Last updated:

12 Dec, 2025 |

5 Minutes Read

Data has always been the backbone of insurance operations. Actuarial models, claims histories, and risk classifications have long guided decision-making. But today, data is more than a support system. It’s the spinal cord of the insurance enterprise—transmitting signals that guide real-time, interconnected decisions.

In this anatomy, data is the spinal cord, coordinating reflexes across the business. Analytics is the brain, processing inputs and directing actions. Systems are the spinal column, providing infrastructure and mobility. Data sources—from customer behavior to telematics and third-party feeds—act as sensory organs, delivering continuous intelligence.

Many insurers still rely on siloed, non-standardized data systems, which hinder the smooth flow of information, slow down decision-making, and increase the organization’s exposure to risk.

In a market defined by dynamic and volatile risks—regulatory shifts, behavioral changes, and emerging technologies—insurance carriers must activate their full nervous system to remain adaptive, precise, and proactive.

To illustrate how a connected data ecosystem drives responsiveness, let’s follow the lifecycle of auto insurance.

From Application to Renewal: How Auto Insurance Responds in Real Time

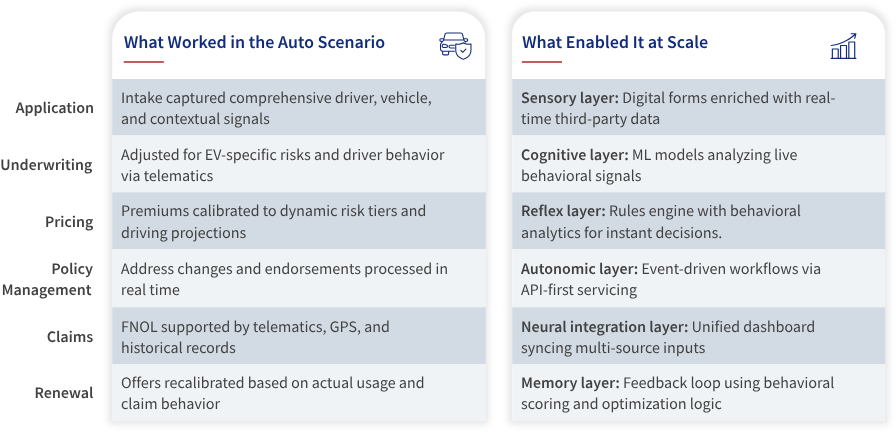

Let’s consider a driver applying for coverage on a new electric vehicle (EV) in an urban area with moderate accident rates but high theft risk. Here’s how each part of the insurance nervous system plays its role.

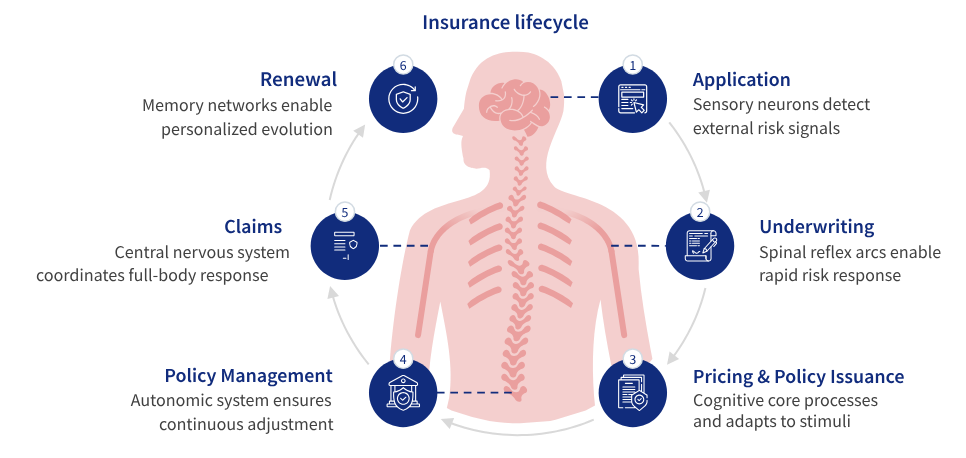

As shown in Exhibit 1, each function—application, underwriting, pricing, claims, and beyond—relies real-time data signals to operate as one connected system.

1. Application: First Signals ReceivedThe journey begins with rich data intake—vehicle specs, driver history, garage location, and telematics opt-ins. These are layered with contextual intelligence like accident density, theft probability, and weather conditions.

Scientific lens: This is the insurer’s sensory network in action—gathering environmental and behavioral inputs for early-stage risk detection. It enhances intake quality, lowers friction, and sets the stage for responsive underwriting.

2. Underwriting: Reflexes Respond to RiskUnderwriters evaluate real-time data inputs—driver behavior, vehicle safety, EV-specific concerns, and usage patterns. Telematics enriches this with live behavior signals.

Scientific lens: Like reflexes triggered by stimuli, underwriting processes must act on credible, current signals, not static profiles. This improves pricing accuracy, reduces claims volatility, and sharpens risk segmentation.

3. Pricing & Policy Issuance: Cognitive Decisions FireRating models process risk tiers, driving trends, and historical claims to calibrate precise premiums. The system dynamically adapts to nuanced risk signals—ensuring policies reflect lived behavior.

Scientific lens: This is the insurer’s cognitive core—analyzing stimuli, scoring risk, and adapting responses in real time. It ensures pricing reflects lived behavior, aligns with underwriting logic, and limits premium leakage through constant recalibration.

4. Policy Management: Real-Time Adjustments TriggeredA mid-policy address change or new driver prompts automatic recalibration. Systems detect, flag, and update the policy—seamlessly and immediately.

Scientific lens: This is the insurer’s autonomic layer—monitoring changes and triggering real-time responses without human input. It ensures seamless servicing, reduces latency, and maintains operational continuity.

5. Claims: The Full System Responds in SyncWhen an accident occurs, the claim ecosystem activates. FNOL is triggered via mobile app, enriched by GPS, telematics, and historical repair data—all feeding into the adjuster’s workflow.

Scientific lens: Like nerve signals routing to the right muscle, claims systems must process multi-source inputs and coordinate a synchronized response. This ensures speed, accuracy, and proactive service recovery.

6. Renewal: The System Learns and RewiresAt term-end, behavioral insights, prior claims, and usage data inform personalized offers—UBI discounts, premium adjustments, or new policy suggestions.

Scientific lens: This is the insurer’s memory and learning function—consolidating past behavior to inform smarter, future-ready decisions. It drives tailored renewals, tighter pricing, and improved retention outcomes.

Operational Excellence in Auto Insurance: What a Responsive Nervous System Delivers

This auto insurance scenario is more than just a process walkthrough—it’s a glimpse into what happens when every part of the insurance enterprise is connected through a responsive data backbone.

Signals travel without friction. Responses are instinctive. Adjustments are automatic. When systems, data, and analytics move in sync, insurers don’t just operate—they adapt in real time.

As shown in Exhibit 2, each lifecycle stage responds to real-time data triggers—just like signals moving through the nervous system.

Optional Strategic Insight

When the enterprise nervous system is connected—sensory inputs, reflex actions, cognitive learning, and infrastructure all aligned—insurance operations don’t just improve; they evolve. That’s the power of activating data at every touchpoint.

Laying the Foundation for the Future

A dashboard doesn’t trigger transformation—it’s sustained by architecture.

To evolve, insurers must prioritize:

- Unified, trusted data: Standardized, validated, and accessible across departments.

- Connected systems: API-first platforms enabling real-time updates and workflow automation.

- Governance by design: Embedded definitions, access controls, and audit readiness.

- Learning loops: Every transaction feed intelligence back into the core for continuous optimization.

Insurers that operationalize this architecture are building resilience—not just efficiency.

Conclusion: Strengthening the Spinal Cord of Insurance

Data is not just a support system—it is the spinal cord of the insurance lifecycle.

It carries critical signals across every function—underwriting, pricing, policy administration, claims, and renewal—coordinating responses with speed and precision. When that spinal cord is strong, insurers move with agility. When it’s disconnected or misaligned, reflexes slow and risks multiply.

This isn’t just about storing data—it’s about activating it, connecting it, and using it to drive better outcomes across the value chain.

And we’re only at the beginning.

In our next post, we’ll explore how insurers can clean, standardize, and govern their data to build a connected, future-ready backbone that supports the full weight of intelligent insurance operations.

Ready to Build a Smarter Insurance Nervous System?

Discover how our BPM insurance solutions help you connect data, systems, and intelligence across the lifecycle. Let’s evolve your operations.